Has the push for ESG-focused funds to divest from fossil fuel companies created an opportunity for less bleeding-hearted investors to make money?

Some seem to think so. There’s “an enormous opportunity for norm-agnostic investors willing to lean against the ESG wave,” the Financial Times wrote last month, pointing to the vast valuation gap between Tesla Inc. and Exxon Mobil Corp. The latter, whose market cap was briefly overtaken by renewables company NextEra Energy Inc. in October, has since rallied with the price of crude and is now worth nearly 80% more. The Global X Renewable Energy Producers ETF, after comfortably outperforming the SPDR Oil & Gas Production & Exploration ETF in each of the past four years, has fallen 15% so far this year. Its oily cousin is up 48%.

The Wages of Sin

A leading renewable power ETF outperformed a leading petroleum ETF for four years. Now it's trailing

Source: Bloomberg

If the conventional theory of sin stocks is correct, investors’ growing aversion to fossil fuels indeed represents represents a golden chance to buy into the same companies. The traditional sectors of alcohol, defense, gambling and tobacco represent a collective $3.15 trillion of market capitalization globally. Fossil fuel companies are together worth nearly twice as much, offering vast scope for sin investors to diversify their portfolios and profit from others’ attempts to decarbonize their savings.

That’s a big if. Indeed, a closer look at sin stocks suggests their outperformance may be no more than a random clustering effect — and the secret of their success may count heavily against companies involved in the very different business of minerals extraction.

The traditional model of sin stock outperformance is that they’re a sort of perpetual value play. The squeamish reluctance of church pension funds and the like to hold such investments pushes down their market price relative to expected returns, allowing less picky investors to buy a stream of good cashflow on the cheap.

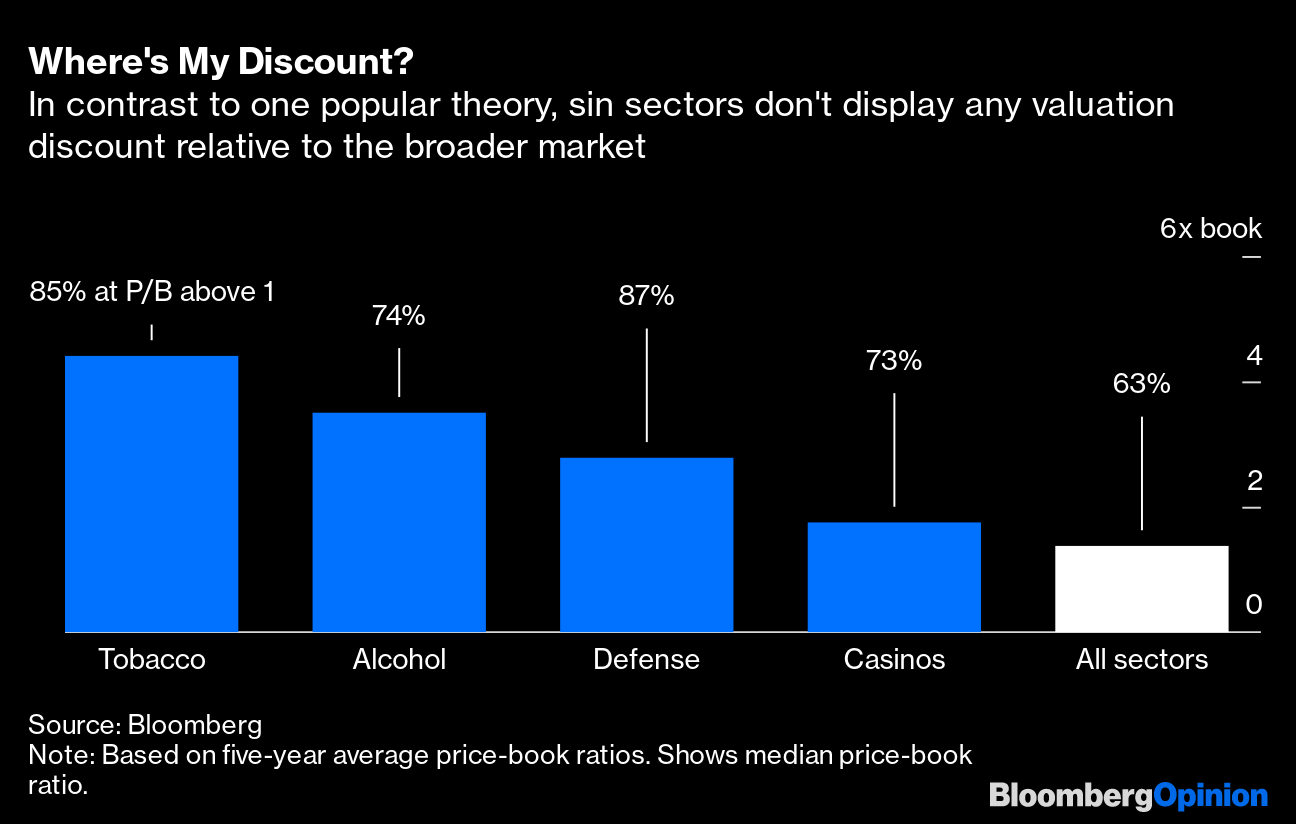

One problem with this theory is that sin stocks are not, in fact, undervalued. All four traditional sin sectors trade at a median five-year average premium to book value higher than the broader market, according to an analysis of more than 33,000 stocks for which Bloomberg has data. Those medians range from a multiple of 1.75 for casinos to 4.4 for tobacco businesses.

Where's My Discount?

In contrast to one popular theory, sin sectors don't display any valuation discount relative to the broader market

Source: Bloomberg

Note: Based on five-year average price-book ratios. Shows median price-book ratio.

Perhaps sin stocks are unusual in another way. After all, they comprise just four of 212 sub-sectors on their level in the Bloomberg Industry Classification Standard. Other qualities they happen to share may be far more decisive in their outperformance than their sinfulness.

“Chance is another explanation,” Eugene Fama, the Nobel economics laureate who originated the most widely cited model of stock pricing with Kenneth French, said by email. A better framework for sin stocks’ outperformance may come from a closer look at the Fama-French model.

Under the latest iteration of that model, stocks that outperform tend to be either undervalued relative to their net assets, a possibility we’ve already ruled out; unusually small; particularly high-margin; or more restrained in their investment spending. The model explains between 71% and 94% of the performance variance between stock portfolios, Fama and French wrote in a 2015 update to the original studies.

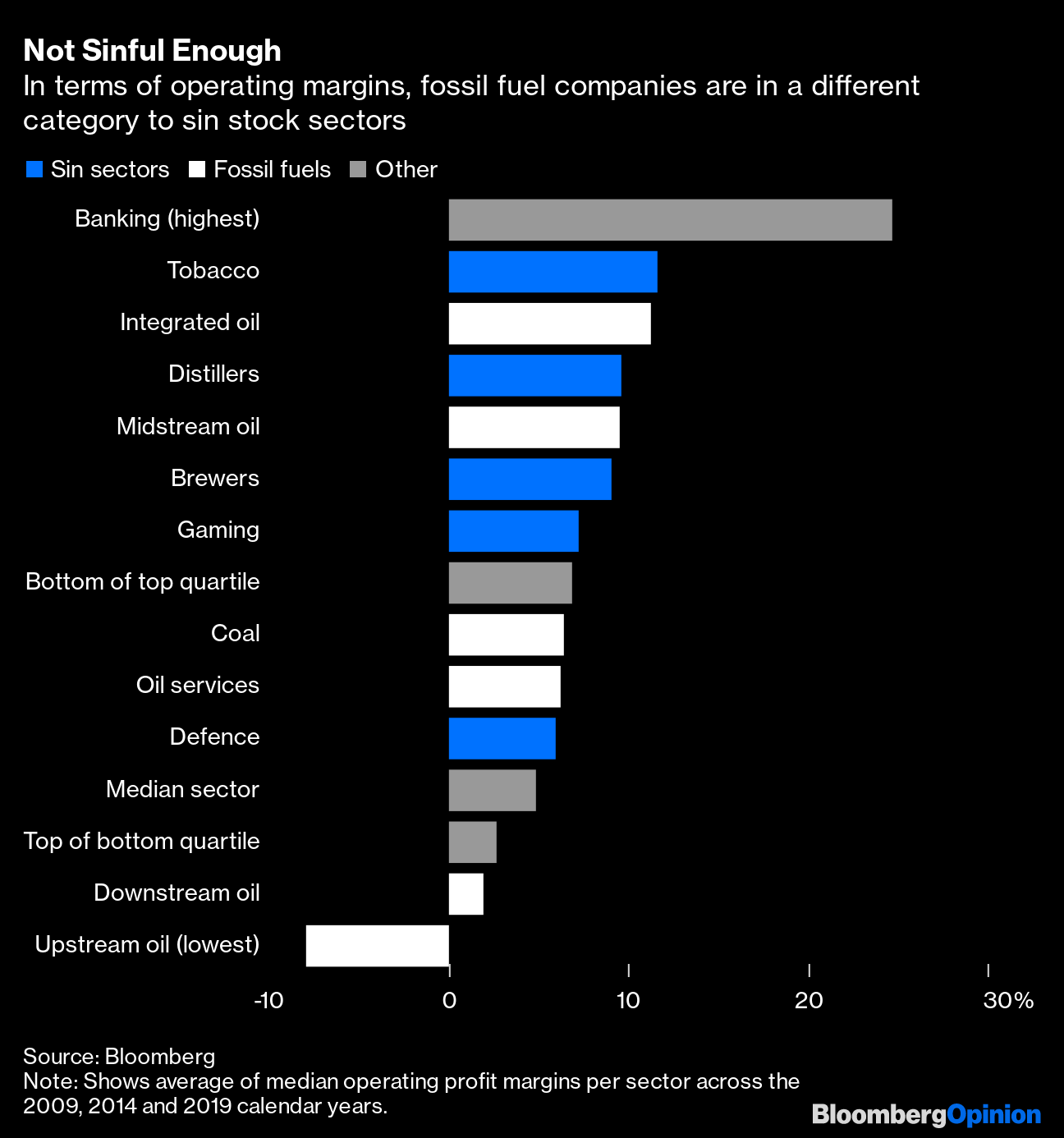

The last two factors are particularly telling. Of 62 sectors for which we compiled data covering the past 10 years, tobacco, distilling, brewing and gambling all came in the top quartile by operating profit margin. Defense companies came in at number 21 on the list. That’s consistent with one other theory about sin stocks, that they prosper because of a lack of competitors willing to enter sectors perceived as being immoral.

Not Sinful Enough

In terms of operating margins, fossil fuel companies are in a different category to sin stock sectors

Source: Bloomberg

Note: Shows average of median operating profit margins per sector across the 2009, 2014 and 2019 calendar years.

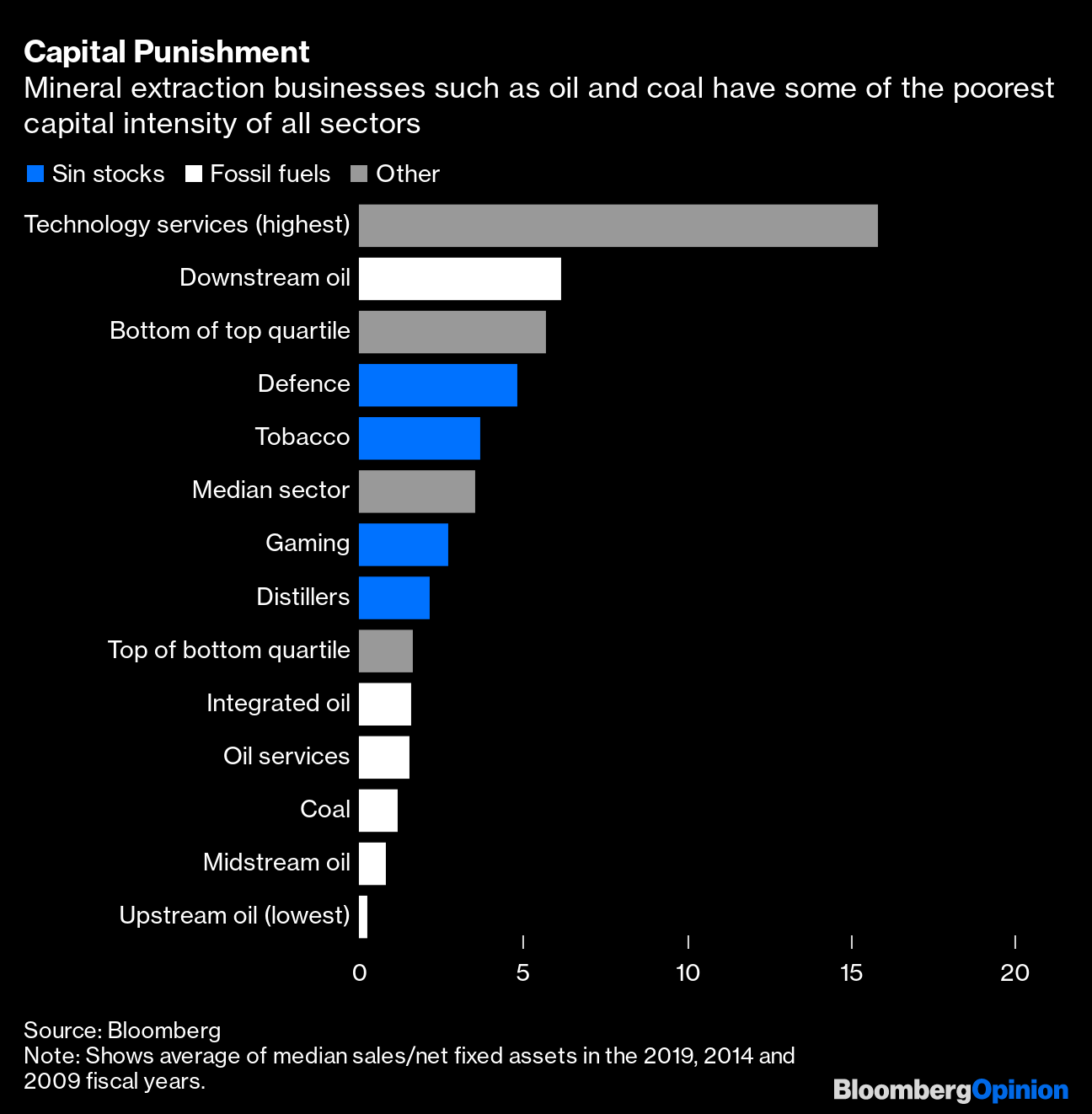

The also tend to perform well in terms of capital intensity. Defense and tobacco came in well above the median on a ranking of sales as a multiple of net fixed assets. Gambling companies were narrowly below the median, while alcohol businesses came lower, in the middle of the second quartile.

Fossil fuel power companies are very different. Upstream and downstream oil businesses have some of the lowest margins of all 62 sectors. Coal and oil services are at similar levels to defense but with far higher capital intensity, while integrated and midstream oil businesses score relatively well in terms of profitability.

The place they perform particularly badly, though, is capital intensity. That’s only natural for businesses whose main assets are mineral reserves that are constantly depleting. Five of the worst-performing sectors in terms of capital usage are upstream, midstream and integrated oil, plus coal and oil services. Only downstream oil refining, which uses the same plant to process crude for decades at a time, performs well on that metric.

Capital Punishment

Mineral extraction businesses such as oil and coal have some of the poorest capital intensity of all sectors

Source: Bloomberg

Note: Shows average of median sales/net fixed assets in the 2019, 2014 and 2009 fiscal years.

That suggests the comparison with traditional sin stocks won’t help the fossil fuel sector. The same attributes that lead alcohol, defense, gambling and tobacco to outperform the market mostly count against businesses involved in resource extraction. Assuming that opprobrium can magically generate outperformance is a strategy that's destined to end in failure.

Crucially, too, the market for alcohol, tobacco, gambling and defense isn’t going away. The first three sectors involve relatively light capital investments to supply consumers who are often quite literally addicted to the product (you might also argue that’s true of defense).

Fossil fuels, by contrast, involve heavy capital commitments in long-term assets to produce a product that the International Energy Agency last week said would decline by 90% (for coal), 75% (oil) or 55% (gas) over the coming three decades if the world is to achieve net-zero carbon emissions.

That’s the very definition of a risky business. If you hope to make sin stock-style returns from that variety of contrarianism, you’d better have a more thought-out justification than simply “fair is foul and foul is fair.”

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the editor responsible for this story:

Rachel Rosenthal at rrosenthal21@bloomberg.net

"fuel" - Google News

May 24, 2021 at 05:00AM

https://ift.tt/3fDHrhW

Why Fossil Fuel Companies Don't Behave Like Sin Stocks - Bloomberg

"fuel" - Google News

https://ift.tt/2WjmVcZ

Bagikan Berita Ini

0 Response to "Why Fossil Fuel Companies Don't Behave Like Sin Stocks - Bloomberg"

Post a Comment